In the global fintech ecosystem, there is often a perception that payment processing itself is the primary driver of profitability. However, a closer examination of leading digital financial platforms suggests that payments primarily serve as an entry point into broader financial ecosystems rather than the core source of earnings.

Companies such as PayPal Holdings Inc., Stripe, Inc., and Block, Inc. illustrate this dynamic clearly. While payment processing enables scale, user acquisition, and transaction flow, a significant portion of long-term value creation tends to emerge from services built on top of these payment rails rather than the transactions themselves.

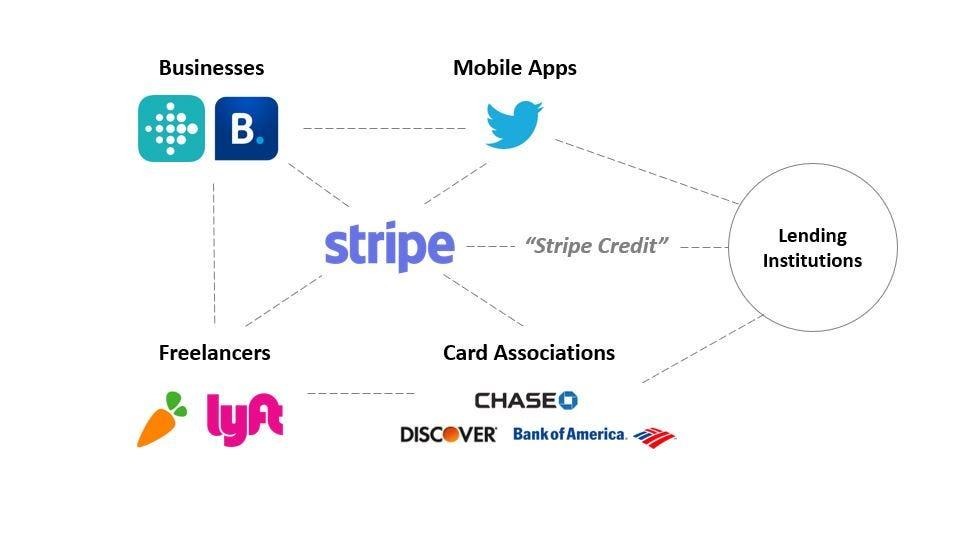

These adjacent services include merchant lending, consumer credit products, foreign exchange services, subscription-based financial tools, fraud management solutions, and analytics-driven merchant services. In many cases, the payments’ function acts as the initial touchpoint that allows these companies to deepen their relationship with users and expand into higher-margin financial products over time.

This structure highlights a clear distinction within fintech business models: payments are characterised by high volume and low unit margins, while layered financial services tend to offer stronger pricing power and more sustainable profitability. The ability of a platform to successfully transition users from basic transactions into credit, savings, or business enablement products becomes a key differentiator in long-term value creation.

From a broader analytical perspective, this also suggests that evaluating fintech companies solely on payment volume or transaction growth can overlook the more meaningful drivers of earnings potential. A more complete assessment involves examining how effectively a platform extends its ecosystem, the depth of product integration across financial services, and the strength of user engagement beyond the initial payment interaction.

An additional layer to this dynamic is the role payments play as an entry point into broader financial ecosystems. In many fintech models, the payment function is not the end product but rather the initial interface through which companies gain access to user behaviour, transaction history, and financial identity. This data becomes increasingly valuable as platforms expand into lending, insurance, wealth management, and business services. In this sense, payments operate as a foundational layer that enables deeper financial intermediation, rather than being the primary source of economic value on their own.

This progression also reflects a broader migration of value within the fintech stack. As payment infrastructure becomes more standardized and increasingly competitive, differentiation appears to shift toward the ability to build integrated financial ecosystems around the user. Platforms that are able to combine payments with credit underwriting, risk assessment, and personalised financial services tend to develop stronger revenue resilience over time. This suggests that long-term performance in fintech may be more closely tied to ecosystem depth and data utilisation rather than transaction processing alone.

Taken together, the global fintech landscape points to a model where payments function primarily as infrastructure, while profitability is increasingly concentrated in financial services layered on top of that infrastructure. The difference between platforms that remain transaction-focused and those that successfully build diversified financial ecosystems appears to be a key determinant of long-term value creation.