Payments as an Entry Point in Fintech Ecosystems

In the global fintech ecosystem, payments rarely act as the main source of profitability. Instead, payment processing often serves as an entry point into broader financial ecosystems. Leading digital platforms show that most long-term value comes from services built on top of payment infrastructure rather than from transactions alone.

Companies such as PayPal Holdings Inc., Stripe, and Block illustrate this structure clearly. Payment systems enable scale, user acquisition, and high transaction flow. However, they generate limited margins on their own. Over time, these platforms shift value creation toward additional financial services that extend beyond basic payments.

Expansion Beyond Core Payment Services

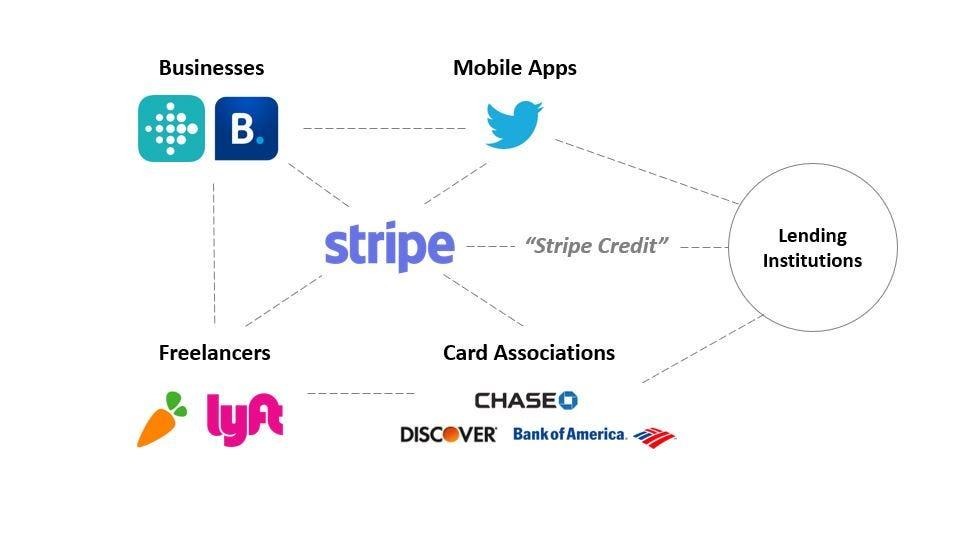

Fintech platforms grow by building services on top of payment rails. These services include merchant lending, consumer credit, foreign exchange tools, subscription-based financial products, fraud detection systems, and data-driven analytics services for merchants. Payments create the first connection with users. After that, platforms expand engagement by offering higher-value financial solutions.

This structure creates a clear separation in fintech business models. Payment services rely on high volume but deliver low margins. In contrast, embedded financial services generate stronger pricing power and more stable profitability. Platforms that successfully move users from basic transactions into credit, savings, or business tools gain a long-term competitive advantage.

Payments as a Data and Distribution Layer

Payments also function as a data collection and distribution layer within fintech ecosystems. They capture user behavior, transaction history, and financial identity. Platforms then use this data to support lending, insurance, wealth management, and other financial services. As a result, payments do not only facilitate transactions but also enable deeper financial intermediation across the ecosystem.

Ecosystem Depth and Value Creation

Fintech performance depends less on transaction volume and more on ecosystem depth. Platforms that integrate payments with credit underwriting, risk management, and personalized financial services tend to achieve stronger and more stable revenue streams. In contrast, platforms that focus only on payment processing often face limited pricing power and weaker long-term margins.

This dynamic reflects a broader shift in the fintech stack. As payment infrastructure becomes more standardized, competitive advantage increasingly depends on the ability to build layered financial ecosystems. Companies that expand successfully beyond payments tend to create more resilient business models over time.

Conclusion

Across the global fintech landscape, payments function primarily as infrastructure rather than a final profit center. Most value creation occurs in financial services built on top of payment systems. Platforms that evolve beyond transaction processing and develop diversified financial ecosystems tend to achieve stronger long-term performance and profitability.