Risk tolerance is a fundamental concept in investing, referring to an individual’s ability and willingness to endure fluctuations in the value of their investments. It plays a critical role in shaping investment decisions, portfolio construction, and long-term financial outcomes. Understanding risk tolerance helps investors align their strategies with their financial goals and emotional comfort levels.

At its core, risk tolerance is influenced by both financial capacity and psychological factors. Financial capacity relates to an investor’s ability to absorb potential losses without compromising their financial stability. This depends on factors such as income, savings, time horizon, and financial obligations. For example, an investor with a stable income and long investment horizon may be better positioned to take on higher risk compared to someone nearing retirement.

On the other hand, psychological tolerance refers to how comfortable an individual is with uncertainty and market volatility. Some investors are able to remain calm during market downturns, while others may feel compelled to sell their investments when prices decline. This emotional response can significantly impact investment outcomes, as decisions driven by fear or panic often lead to losses or missed recovery opportunities.

Risk tolerance typically falls into three broad categories: conservative, moderate, and aggressive. Conservative investors prioritize capital preservation and tend to prefer low-risk investments such as fixed income securities. Moderate investors seek a balance between risk and return, often combining equities and bonds in their portfolios. Aggressive investors are more willing to accept higher levels of risk in pursuit of greater returns, often allocating a larger portion of their portfolio to equities or growth-oriented assets.

Time horizon is closely linked to risk tolerance. Investors with longer time horizons generally have a greater capacity to take on risk because they have more time to recover from market downturns. Short-term investors, on the other hand, may need to prioritize stability to avoid losses that could affect near-term financial needs. Aligning investment strategy with time horizon helps ensure that risk exposure remains appropriate.

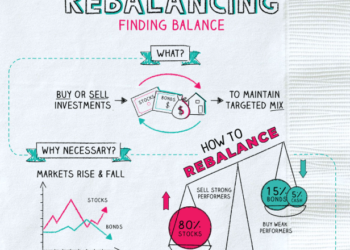

Diversification is an important tool in managing risk tolerance. By spreading investments across different asset classes, sectors, or geographic regions, investors can reduce the impact of poor performance in any single investment. Diversification does not eliminate risk entirely, but it helps create a more balanced and resilient portfolio.

It is also important to recognize that risk tolerance is not static. It can change over time due to shifts in financial circumstances, life events, or market conditions. For instance, an investor may become more conservative after experiencing significant losses or as they approach a major financial goal. Regularly reviewing and adjusting investment strategies ensures that they remain aligned with current risk tolerance.

A mismatch between risk tolerance and investment strategy can lead to poor outcomes. Taking on too much risk may result in stress and impulsive decisions during market volatility, while being overly conservative may limit potential returns and hinder long-term growth. Achieving the right balance is essential for maintaining consistency and discipline in investing.

In conclusion, risk tolerance is a key factor in successful investing, influencing how investors approach opportunities and manage uncertainty. By understanding both their financial capacity and emotional comfort with risk, individuals can make more informed decisions and build portfolios that support their long-term objectives