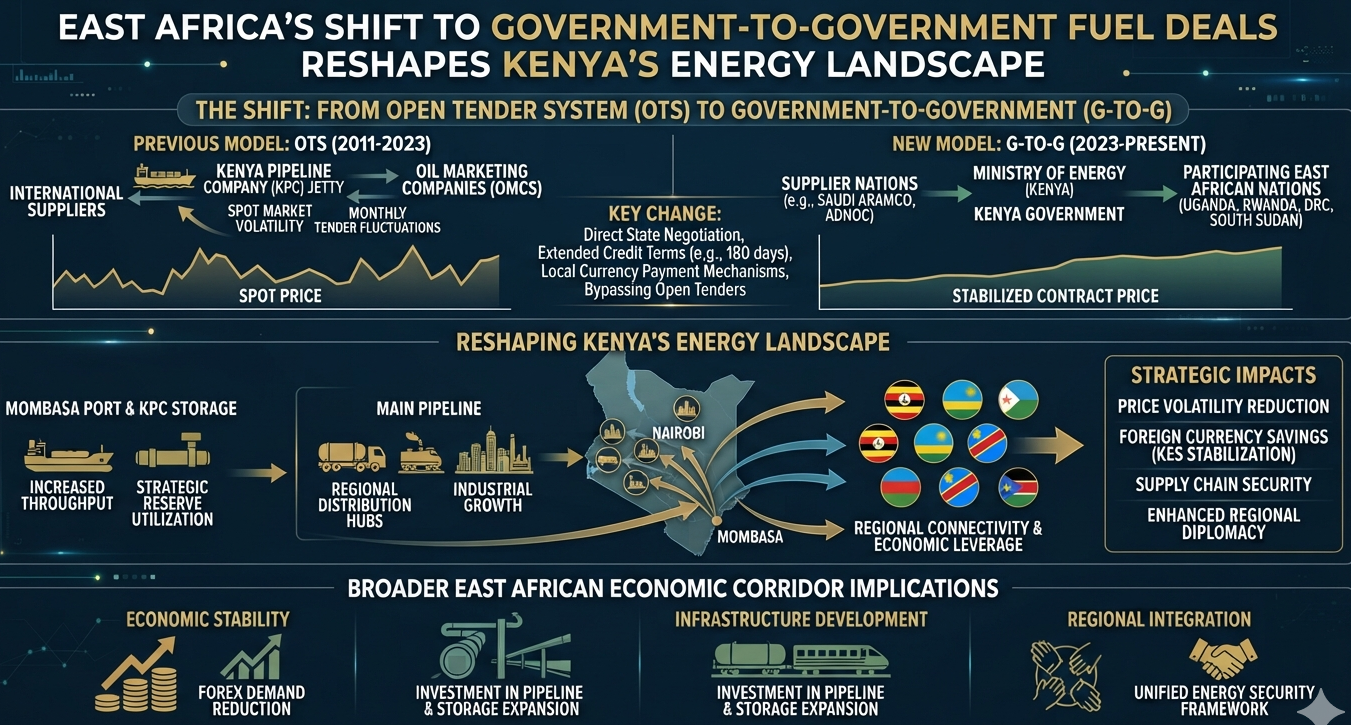

East Africa’s petroleum market is undergoing a significant structural transition as regional governments increasingly move towards government-to-government (G-to-G) fuel procurement arrangements. Rwanda’s decision to implement the model from August 2026 represents the latest development in a trend that has already transformed fuel supply dynamics in Kenya and Uganda. The transition signals a gradual departure from traditional private-sector-led fuel importation and introduces a new competitive environment for regional energy players.

Under the new framework, Rwanda’s fuel imports will be handled directly by the Rwanda National Petroleum Corporation through a supply arrangement with OQ Trading, the international trading subsidiary of the Sultanate of Oman. The move effectively reduces the role previously played by Kenyan oil marketing companies in supplying petroleum products destined for the Rwandan market, thereby diminishing an important source of transit fuel revenues for the sector.

For Kenya’s downstream petroleum industry, the implications are substantial. Transit fuel trading has historically provided stable revenue streams for local marketers, supported by Kenya’s strategic position as a regional logistics hub through the Northern Corridor. However, the earlier transition of Uganda to a similar procurement arrangement had already reduced market volumes for Kenyan firms. Rwanda’s adoption of the same model further narrows the addressable transit market, leaving oil marketers increasingly dependent on destinations such as the Democratic Republic of Congo, Burundi, and South Sudan.

This concentration of market exposure introduces additional risks. Lower trading volumes may reduce economies of scale within the sector, compress operating margins, and accelerate consolidation among petroleum marketers seeking to preserve profitability in a changing business environment. Companies with significant exposure to transit fuel sales are therefore likely to face greater earnings pressure in the medium term.

Despite these challenges, the transition presents a more favorable outlook for Kenya’s energy infrastructure segment. Rwanda is expected to continue utilizing the Port of Mombasa as its primary import gateway while maintaining reliance on the Kenya Pipeline Company (KPC) network for fuel transportation and storage services. As a result, throughput volumes within the pipeline system and associated storage facilities are expected to remain relatively resilient even as the role of private intermediaries declines.

The resilience of infrastructure demand is further reinforced by Rwanda’s acquisition of a minority stake in KPC, a development that strengthens long-term commitment to the Northern Corridor route and supports deeper regional cooperation in energy logistics. Stable demand for transportation and storage services could help cushion infrastructure operators from the revenue pressures affecting fuel traders.

The broader regional trend reflects governments’ desire to strengthen energy security and improve macroeconomic stability. G-to-G procurement frameworks allow countries to negotiate directly with international suppliers, potentially securing longer credit periods, reducing immediate foreign exchange requirements, and improving resilience during periods of global supply disruptions. Kenya introduced its own G-to-G arrangement in 2023 primarily to reduce pressure on the Kenyan shilling and stabilize domestic fuel supply, while Uganda and Rwanda have pursued similar objectives centered on supply reliability and cost management.

The evolution of East Africa’s fuel supply chain therefore represents more than a change in procurement practices; it signals a fundamental restructuring of the region’s petroleum trade model. As traditional fuel trading opportunities become more limited, investment interest is likely to shift increasingly towards logistics infrastructure, storage facilities, pipeline transportation, and regional energy integration projects.

For investors and industry participants, the emerging landscape suggests a divergence in fortunes across the sector. Infrastructure operators such as KPC appear well positioned to benefit from sustained demand for strategic assets, while businesses heavily reliant on transit fuel marketing may need to diversify operations and adapt their business models to remain competitive in a rapidly evolving regional energy market.