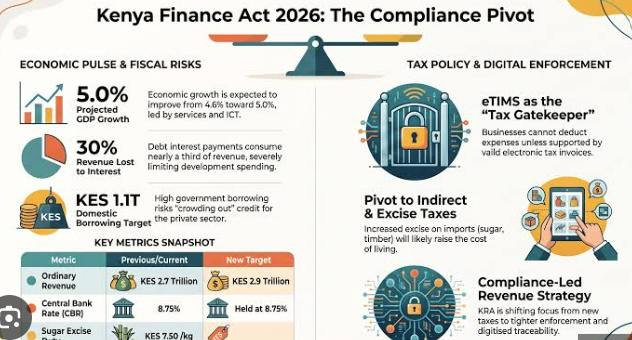

The enactment of Kenya’s Finance Act 2026 marks one of the most significant fiscal policy developments in recent years, providing the revenue framework required to support the government’s KSh4.8 trillion budget for the 2026/27 financial year. The legislation reflects a broader policy shift towards increasing domestic revenue mobilization as Kenya seeks to reduce reliance on external borrowing and strengthen fiscal sustainability.

The government’s strategy centers on expanding the tax base, improving compliance, and enhancing tax administration efficiency. Advances in digital tax systems and data analytics are expected to improve revenue collection by reducing leakages and identifying previously untaxed economic activity. In parallel, reforms to the tax dispute resolution process aim to reduce delays associated with lengthy litigation, allowing contested tax matters to be resolved more efficiently and improving revenue predictability for the exchequer.

Importantly, several proposals that had generated significant public concern were not included in the final legislation. Widely discussed measures affecting freehold land ownership, second-hand clothing imports, and mobile money transactions were ultimately excluded, limiting the immediate burden on lower-income households and informal sector participants who rely heavily on these economic activities.

Nevertheless, the Finance Act introduces several measures that are likely to have meaningful economic implications for households and businesses. Among the most notable changes is the increase in the residential rental income tax rate from 7.5% to 10.0%, representing an increase of 2.5 percentage points. The measure is intended to improve tax compliance within the property sector, although concerns remain that part of the additional tax burden could be transferred to tenants through higher rental charges, particularly in urban centers already experiencing housing affordability pressures.

The legislation also introduces a more demanding compliance environment for businesses through revised tax administration timelines. Corporate and individual income tax filing deadlines have been brought forward from 30 June to 30 April, requiring businesses and taxpayers to adjust reporting and financial planning processes accordingly.

Further changes affect Kenya’s rapidly expanding digital economy. The Act broadens the application of withholding taxes to cover selected digital payments, platform-based financial services, and merchant interchange fees, while also tightening Value Added Tax treatment on electronic payment processing services. These measures are expected to increase compliance obligations for financial technology companies, digital platforms, and payment service providers operating within Kenya’s increasingly cashless economy.

From a policy perspective, the Finance Act 2026 reflects the difficult balance between raising revenue and supporting economic growth. While stronger domestic revenue generation can improve fiscal sustainability and reduce borrowing requirements, higher taxes and increased compliance costs may place pressure on household incomes, business profitability, and investment activity in the short term.

The long-term effectiveness of the legislation will therefore depend not only on revenue collection outcomes but also on the ability of the economy to absorb the additional tax burden without undermining competitiveness, private sector expansion, and consumer spending.