Data-Driven Lending and the Transformation of Credit Assessment Systems

Data-driven lending and access to credit has historically depended on conventional underwriting systems based on income verification, collateral requirements, and credit bureau records. In the early 2000s and the early 2010s, lenders relied on manual documentation and in-person verification to make credit decisions. As a result, access to formal credit remained limited, especially for individuals in informal economic sectors where financial records were incomplete or unavailable. However, as financial systems evolved in the late 2010s and early 2020s, digitization of economic activity enabled new credit models built on digital data sources.

The Emergence of Data-Driven Lending Models

Data-driven lending refers to credit evaluation methods that use transactional data, behavioral indicators, and non-traditional financial metrics to assess borrower risk. Initially, lenders in the mid-to-late 2010s incorporated mobile usage data, digital payment histories, and utility payment records into early credit scoring systems. Later, by the early 2020s, these models shifted toward real-time systems that continuously update credit scores, and this reduced dependence on static and periodically refreshed assessments.

Mobile Money Ecosystems and Credit Expansion in Kenya

In Kenya, this transformation closely followed the expansion of mobile money infrastructure, especially through Safaricom’s M-Pesa ecosystem, which expanded significantly between 2015 and 2024. In this context, the system generated large-scale transaction datasets that enabled detailed analysis of income inflows, spending behavior, and liquidity patterns. As a result, these datasets supported the growth of digital credit products such as M-Shwari (2012), KCB M-Pesa (2015), Tala (expanded from around 2014), Branch, and Fuliza (2019). Importantly, Fuliza uses M-Pesa transaction history to provide overdraft facilities, which reflects a shift toward continuous credit evaluation rather than single-point loan assessment.

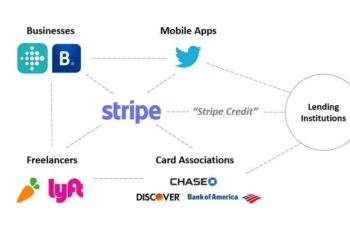

Global Adoption of Platform-Based Credit Systems

Globally, similar developments emerged within digital financial platforms. For example, in the early 2010s, PayPal introduced lending products based on merchant transaction history. Similarly, in the late 2010s and early 2020s, Square (now Block Inc.) expanded its lending operations by using real-time sales data from small businesses to assess credit eligibility and automate loan issuance within its ecosystem. In addition, Amazon expanded merchant lending between 2018 and 2023 by using internal platform metrics such as sales performance, inventory turnover, and customer engagement data to determine credit limits and repayment capacity. Collectively, these examples show a broader shift toward credit systems embedded within digital platforms and powered by proprietary datasets.

Artificial Intelligence and Real-Time Credit Scoring

Between 2020 and 2026, artificial intelligence and machine learning significantly expanded the capability of credit scoring systems. These systems now process large volumes of structured and unstructured data in near real time. Consequently, credit models have shifted from periodic scoring updates to dynamic systems that adjust credit limits and pricing based on continuous behavioral inputs derived from digital activity.

Structural Shift in Credit Allocation Systems

Credit allocation now relies more on transaction-level data than traditional financial documentation. In emerging markets, this shift aligns with broader financial digitization, where economic activity is increasingly captured through mobile and digital platforms. As a result, the availability of alternative data for credit assessment has expanded significantly, especially in economies with large informal sectors.

Investment Implications and Risk Considerations

From an investment perspective, lending models increasingly incorporate data infrastructure and platform ecosystems into credit origination strategies. Over the period from 2010 to 2026, lenders progressively integrated higher-frequency data sources into risk assessment frameworks. At the same time, new risks have emerged, including data governance challenges, model dependency, and sensitivity to macroeconomic shifts that affect the reliability of behavioral data in credit systems.

Conclusion

Overall, data-driven lending reflects a structural shift in credit assessment from static, document-based evaluation toward continuous analysis of transactional behavior within digital ecosystems. This transformation has been enabled by the expansion of digital payments infrastructure, improved data availability, and advances in computational credit modeling systems.