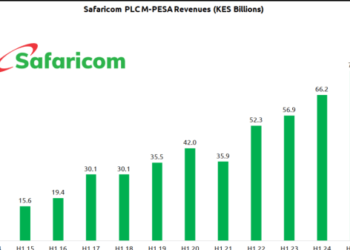

Kenya has continued to strengthen its position as one of the world’s leading digital financial markets, supported by widespread mobile money adoption and an expanding cashless payment ecosystem. Mobile merchant payments have experienced sustained growth, with transaction volumes largely driven by Safaricom’s Lipa na M-Pesa platform. This expansion has significantly increased mobile retail transaction throughput, reinforcing Kenya’s reputation as a global leader in digital financial inclusion and technology-driven financial services.

Despite this strong transaction growth, the country’s fintech landscape is entering a new phase shaped by evolving regulatory reforms. The Central Bank of Kenya (CBK) has intensified the implementation of full cross-wallet interoperability, while the Capital Markets Authority (CMA) continues to strengthen oversight of digital investment and wealth management sandboxes. Together, these regulatory developments are reshaping competition within the financial technology sector by reducing merchant payment processing margins and encouraging greater market openness.

The implementation of merchant-level interoperability represents a significant structural shift within Kenya’s digital payments industry. Historically, dominant mobile money providers benefited from closed payment ecosystems that enabled them to retain customers within proprietary merchant networks while charging relatively higher transaction fees. Under the interoperable framework, consumers can now use different mobile wallets or commercial banking applications to complete transactions through standardized merchant payment channels such as universal QR codes and merchant till numbers. As a result, payment infrastructure is increasingly functioning as shared financial infrastructure rather than as exclusive proprietary networks.

This transition has important implications for fintech profitability. While transaction volumes continue to expand, payment processing has become a lower-margin business due to increased competition and standardized access across providers. Revenue generation can therefore no longer rely primarily on merchant transaction fees. Instead, financial technology firms are being encouraged to diversify their income streams by developing higher-value digital financial products and services.

Many operators are responding by expanding embedded financial solutions within their payment ecosystems. These include digital micro-insurance products, merchant financing supported by transaction data, cross-border remittance services, and other integrated financial solutions that generate stronger margins than traditional payment processing. At the same time, investments in advanced customer analytics and proprietary digital credit-scoring capabilities are becoming increasingly important in supporting personalized financial products and improving customer lifetime value.

From an investment perspective, the changing operating environment suggests that transaction volume alone is no longer a sufficient measure of fintech performance. Investors and equity analysts are placing greater emphasis on Average Revenue Per User (ARPU), particularly revenue generated through value-added digital services rather than basic payment switching activities. This shift reflects the growing importance of customer engagement, ecosystem integration, and product diversification in determining long-term financial performance.

Business-to-business digital solutions are also emerging as an important source of sustainable growth. Fintech companies that successfully expand merchant software-as-a-service (SaaS) platforms can deepen relationships with businesses by offering integrated payment acceptance, inventory management, financial reporting and financing solutions within a single digital ecosystem. These services create additional recurring revenue opportunities while strengthening merchant retention.

Overall, Kenya’s digital payments market continues to demonstrate robust structural growth as consumers increasingly embrace cashless transactions. However, regulatory reforms are transforming the industry’s competitive dynamics by reducing reliance on proprietary payment networks and encouraging greater interoperability. As payment processing becomes increasingly commoditized, future growth will depend on innovation, data-driven financial services and the successful integration of high-value digital products. Institutions capable of building comprehensive financial ecosystems beyond basic payment infrastructure are likely to be better positioned to sustain profitability and long-term growth in Kenya’s evolving fintech sector.