Safaricom has officially introduced Shiriki Pay, a new feature within M-Pesa that allows users to share and manage money collectively. The launch marks another evolution in Kenya’s mobile money ecosystem, shifting from purely individual wallets to controlled shared spending.

The feature enables one M-Pesa user to create a shared spending arrangement with trusted individuals, such as family members, business partners, or colleagues, while maintaining oversight of how funds are used.

What Shiriki Pay Does

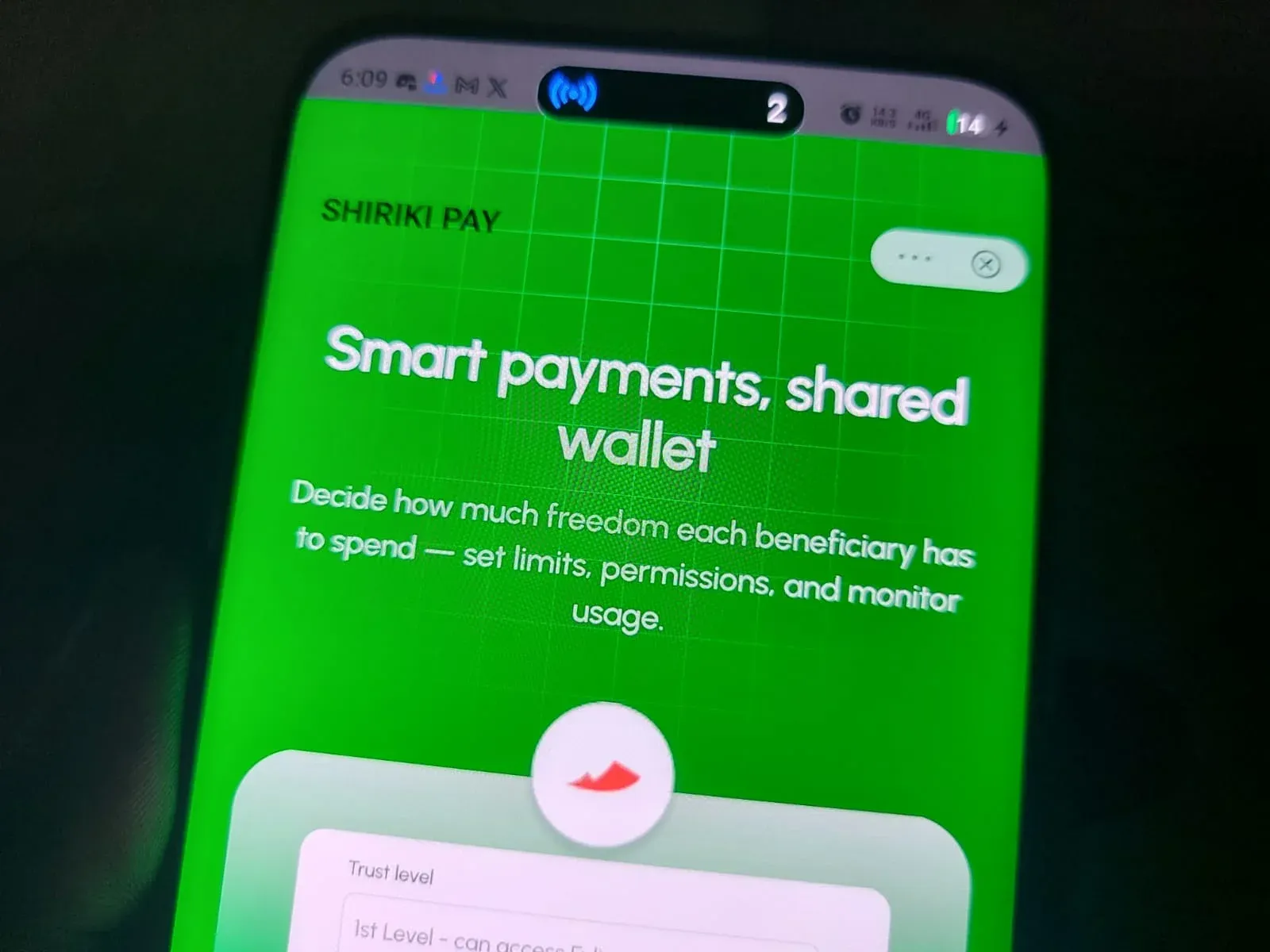

Shiriki Pay functions as a controlled shared wallet. A primary account holder can allocate funds for shared use, set spending limits, and monitor transactions in real time. Instead of sending money multiple times for school fees, shopping, or household expenses, users can create a structured spending channel within M-Pesa itself.

This means:

-

Parents can allocate funds to children with usage limits

-

Couples can manage joint expenses transparently (which definitely is a preferred option, especially this love season)

-

Small business teams can control operational spending

-

Chamas or informal groups can manage shared contributions

Importantly, the main wallet owner retains control and visibility, reducing the risk of misuse while improving accountability.

Why It Is Relevant to Kenyans

Mobile money is deeply embedded in Kenya’s daily life. With Safaricom’s, arguably the biggest telecommunications company in East and Central Africa, from sending money to paying for expenses, M-Pesa is often the primary financial tool for millions. However, shared financial responsibilities have traditionally required informal arrangements, sending money manually, or trusting recipients to use it responsibly.

Shiriki Pay addresses this gap by introducing structure into shared finances. For families managing budgets, small businesses controlling petty cash, or group savings initiatives requiring transparency into spending, the feature adds convenience and oversight.

It also aligns with Kenya’s growing demand for smarter digital financial tools as more people seek efficiency, security, and financial discipline in everyday transactions.

Loopholes It Seeks to Address

Before Shiriki Pay, common challenges included:

-

Repeated transfers for routine shared expenses

-

Limited control over how transferred funds were spent

-

Lack of transparency in group spending

-

Informal trust-based arrangements that were prone to disputes

By centralizing shared spending within one monitored structure, Shiriki Pay aims to reduce misuse, improve record-keeping, and streamline collaborative financial management.

Potential Drawbacks and Risks

Despite its innovation, Shiriki Pay may present some concerns.

First, privacy considerations arise. Shared wallet monitoring means the primary holder can track all transactions, which could create tensions in sensitive financial relationships.

Second, there may be risks if access permissions are not properly managed. If login credentials or device access are compromised, shared funds could become vulnerable. This has been a topic of continuous concern, especially with the telecommunication giant at the core of most transactions and “extremely” confidential information for most Kenyans.

Additionally, digital literacy gaps could limit adoption among older or less tech-savvy users. Understanding limits, permissions, and monitoring tools requires a certain level of familiarity with mobile financial systems.

Even as more developments, innovations, and inventions take place, a core factor is always the audience. Do they understand the feature? Do they have access to educational information that promotes comprehension of the faults, weaknesses, and advantages of these systems?

Finally, like all centralized digital solutions, the feature depends entirely on system reliability. Any technical glitches could temporarily disrupt shared access. With the feature involving finance, a key aspect of every Kenyan’s life is liquidity, and express client support. If I can’t access it, then I must reach out to someone who will answer why.

A Step Toward Smarter Digital Finance

Overall, Shiriki Pay reflects the continued evolution of Kenya’s fintech landscape. By moving beyond simple peer-to-peer transfers into structured shared spending, Safaricom is responding to changing financial behaviors among users.

Whether it becomes widely adopted will depend on user trust, ease of use, and how effectively it balances convenience with security.

This article draws on personal research with attribution to the following sources:

https://www.dawan.africa/news/safaricom-launches-shiriki-pay-controlled-shared-m-pesa-spendinghttps://medium.com/activated-thinker/shiriki-pay-explained-smart-convenience-or-a-risky-shortcut-b0fda3fa00a6https://techweez.com/2026/01/22/safaricom-shiriki-pay-share-m-pesa-wallet/#google_vignette