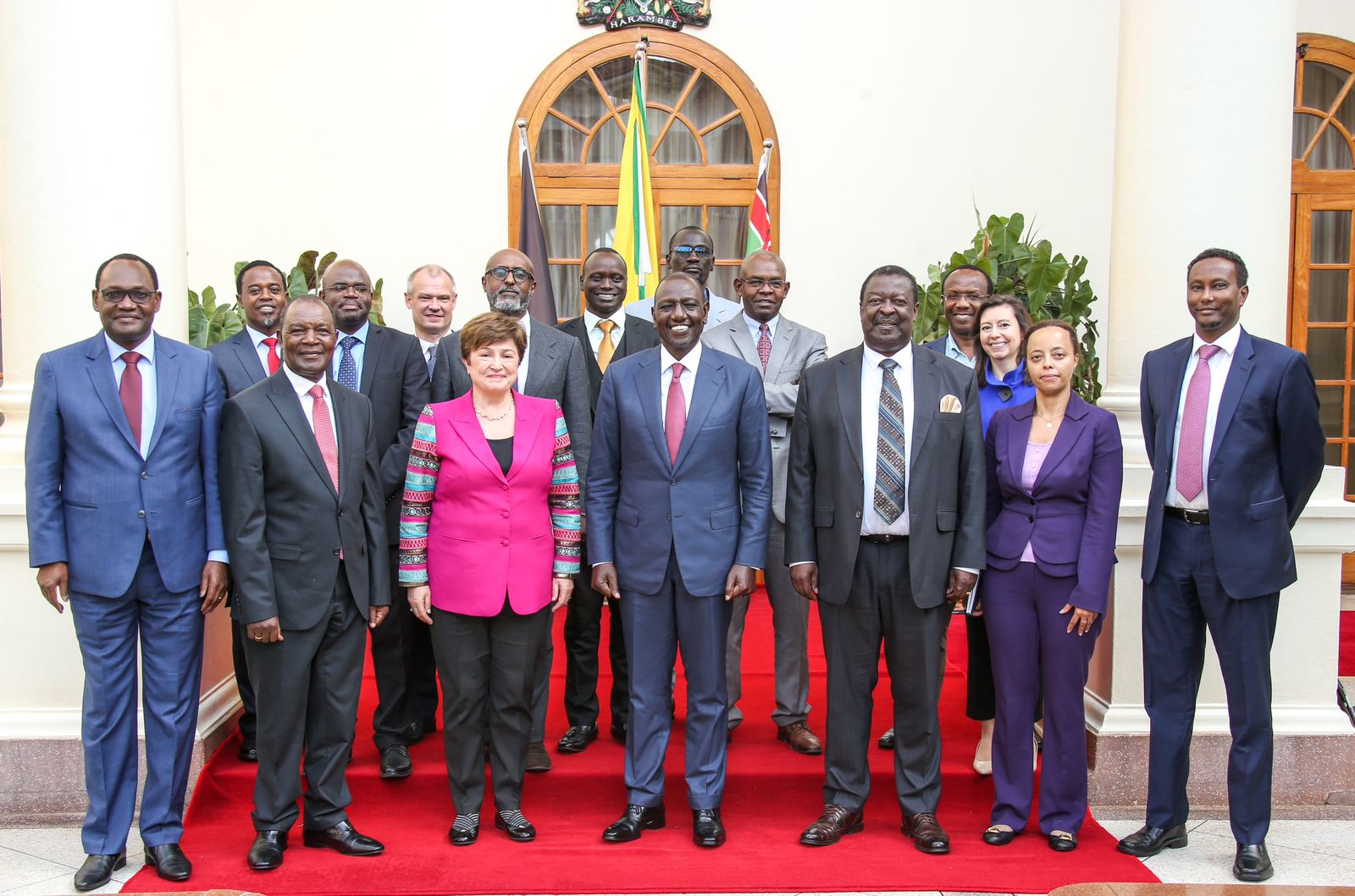

International Monetary Fund managing director Kristalina Georgieva dispels fears of Kenya defaulting on Eurobond debt which matures next year.

She spoke during a media roundtable on Thursday last week in-between her busy tour of Nairobi as the IMF revealed that Kenya stands to get an additional Kshs 41 billion from the IMF when it completes its mission review next week.

The appreciation of the dollar has greatly affected the Kenyan economy. The depreciation of the currencies overall is the highest we have seen in 20 years. So there is an impact, leading to debt distress.

Georgieva noted that they don’t foresee a systemic debt crisis, because the countries that are at the point of needing debt restructuring are still a relatively small group. Kenya is definitely not among them. Kenya’s debt is sustainable but indeed the country finds itself cut off from the international markets and the domestic market needs a bit of help to function at a higher level.

Read:Kenya to Record 5.3 Percent Economic Growth – IMF

“It would be good to see more attention paid and we discussed this with the Central Bank of Kenya on how to make the domestic market more vibrant. That is, of course, related to bond issuance domestically with a reward for those who buy bonds being at a more attractive level,” she added.

IMF boss also pointed out the fact that they do not see Kenya facing difficulties to serve the USD 2.0 billion next year, attributing this to reserves being still quite sound.

Kenya has USD 6.4 billion in reserves and it has been taking very prudent measures both on the fiscal front and on the monetary policy side to make sure that this reserve position remains sound.

In addition, Kenya can raise money through syndicated loans or other ways including from IMF.

Email your news TIPS to editor@thesharpdaily.com