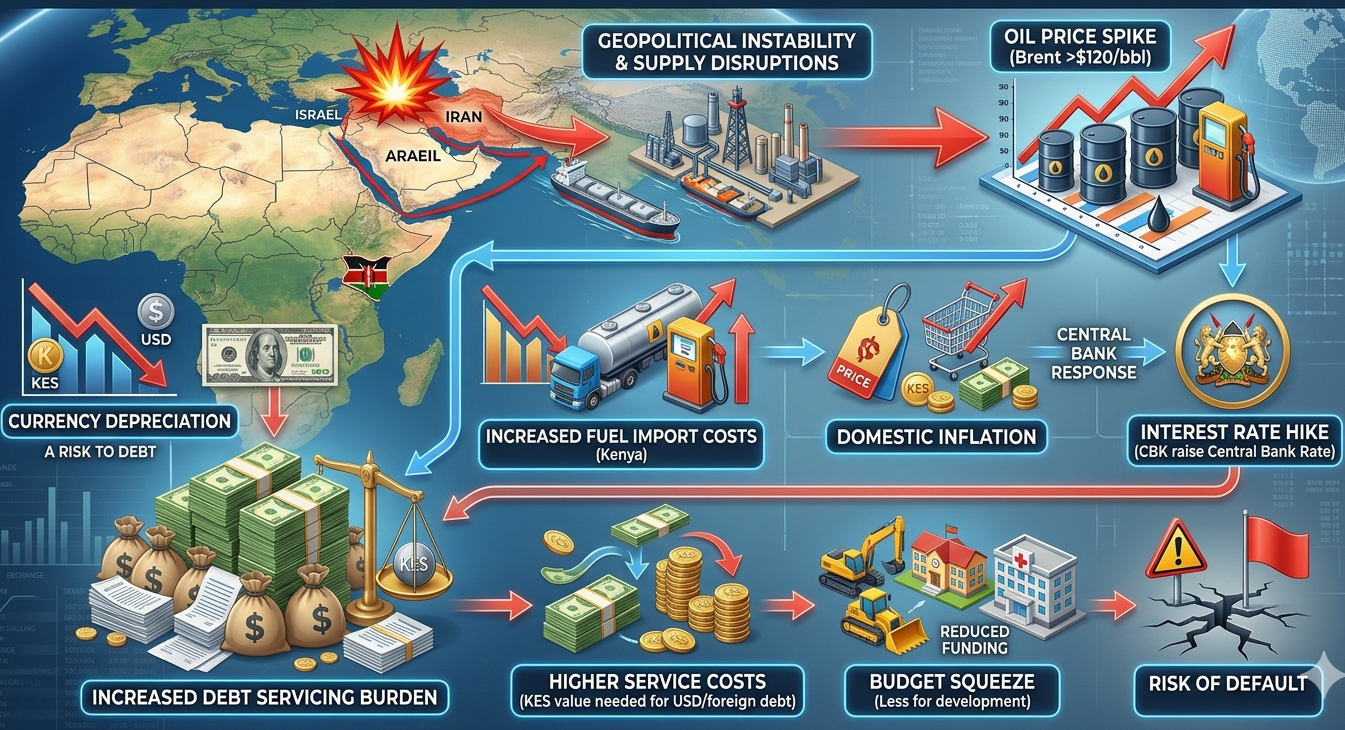

The escalation of tensions between Iran and Israel is introducing new risks to the global economy, with emerging markets becoming increasingly vulnerable to the indirect effects of geopolitical instability. Although Kenya has no direct involvement in the conflict, the country’s dependence on imported fuel and foreign-denominated borrowing means developments in the Middle East have the potential to significantly influence its fiscal position and debt sustainability outlook.

One of the most immediate channels through which the conflict affects Kenya is the international oil market. The Middle East remains the world’s dominant oil-producing region and hosts critical shipping routes that facilitate global energy trade. Among these, the Strait of Hormuz serves as one of the most strategically important transit corridors for crude oil exports. Any disruption to shipping activity or concerns over supply security in the region typically translate into higher global energy prices and increased market volatility.

For Kenya, rising crude oil prices create substantial macroeconomic pressures. As a net importer of petroleum products, higher international prices increase the country’s fuel import bill and raise demand for foreign currency to finance purchases. This exerts pressure on foreign exchange reserves and contributes to depreciation of the Kenyan shilling against major global currencies, particularly the United States dollar.

Exchange rate movements carry significant implications for public debt management. A considerable share of Kenya’s public debt portfolio is denominated in foreign currencies, with obligations largely linked to the United States dollar and other international currencies. Consequently, any weakening of the shilling increases the local currency cost of servicing external debt repayments, even when the nominal value of the debt remains unchanged. This creates additional pressure on government finances and can complicate fiscal consolidation efforts.

The conflict may also influence global monetary policy conditions. Higher energy prices often contribute to inflationary pressures across advanced economies, potentially encouraging central banks to maintain restrictive monetary policies for longer periods. Delays in interest rate reductions would sustain elevated global borrowing costs and limit access to affordable financing for frontier markets and developing economies.

For Kenya, prolonged periods of high international interest rates could increase refinancing costs for existing obligations and make future external borrowing more expensive. The country already allocates a significant proportion of government revenues towards interest payments, reducing the fiscal space available for infrastructure investment, public services, and social programmes. Additional increases in borrowing costs would further constrain budgetary flexibility.

Global investor behavior represents another important transmission mechanism. Periods of geopolitical uncertainty often trigger a reallocation of capital towards lower-risk assets such as United States Treasury securities and other safe-haven investments. This shift can reduce capital inflows into frontier markets and increase the risk premium demanded by investors when purchasing sovereign debt issued by emerging economies.

In practical terms, this could translate into higher yields on Kenyan sovereign bonds and increased costs associated with raising capital from international markets. Reduced investor appetite for frontier-market assets may also heighten exchange rate volatility and further increase external financing risks.

Although Kenya cannot directly influence geopolitical developments in the Middle East, several policy measures could strengthen economic resilience. Continued fiscal discipline, exchange rate stabilization efforts, and prudent debt management strategies remain essential in limiting exposure to external shocks. At the same time, expanding investments in renewable energy generation and reducing dependence on imported petroleum products would lower vulnerability to future commodity price disruptions.

The Iran–Israel conflict therefore extends beyond foreign policy considerations for Kenya. It highlights the extent to which geopolitical tensions can transmit rapidly through commodity markets, financial systems, and capital flows, ultimately affecting domestic fiscal stability. As Kenya continues to manage a sizeable external debt burden, maintaining resilience against global shocks will remain a critical component of long-term debt sustainability.