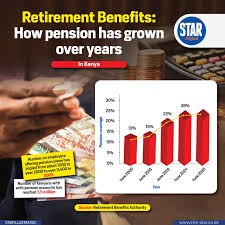

Pension funds are among the largest pools of long-term capital in Kenya, holding trillions of shillings on behalf of current and future retirees. By design, these funds are meant to invest patiently, support long-term growth, and provide stable retirement incomes. Yet a growing debate has emerged on whether Kenyan pension funds too conservative for an economy that needs long-term risk capital.

On one hand, caution is understandable. Pension funds have a fiduciary duty to protect members’ savings. Regulatory frameworks emphasize capital preservation, liquidity, and predictable returns. As a result, most Kenyan pension schemes allocate heavily to government securities, fixed income instruments, and listed equities. These assets offer relative safety, transparency, and ease of valuation, critical factors for institutions responsible for retirement income.

However, this conservative posture comes at a cost. Kenya’s economy faces persistent financing gaps in infrastructure, housing, manufacturing, private equity, and climate-related projects, sectors that require long-term capital and are poorly served by short-term bank lending. Pension funds, with their long investment horizons, are theoretically well placed to fill this gap. Yet in practice, allocations to alternative assets remain modest.

The concern is not that pension funds are risk-averse, but that they may be overly concentrated in traditional assets. Heavy exposure to government securities ties pension performance closely to fiscal conditions and interest rate cycles. In periods of low yields, real returns can be eroded by inflation, undermining the long-term purchasing power of retirement savings.

To be fair, progress has been made. Regulatory reforms have gradually allowed pension schemes to invest in private equity, real estate investment trusts, infrastructure projects, and asset-backed securities. A number of funds have begun exploring these opportunities, often through collective investment vehicles that reduce risk and improve governance. Still, uptake remains uneven, particularly among smaller schemes with limited expertise.

The challenge lies in balancing innovation with prudence. Alternative investments are complex, less liquid, and harder to value. Without strong governance, professional management, and clear risk controls, such investments can expose pension funds to losses that undermine member confidence. This explains why many trustees remain cautious.

The question, therefore, is not whether pension funds should take excessive risk, but whether they are fully utilizing their long-term nature. With the right safeguards, diversification into productive sectors could enhance returns, support economic growth, and reduce overreliance on government debt.

Ultimately, Kenya’s pension funds are neither too conservative nor too aggressive by default. The real issue is capability. As governance standards improve and investment expertise deepens, pension funds can play a more active role in financing the country’s growth, without compromising the security of retirees’ savings.