Public enterprises have traditionally operated under a different logic than private corporations. Their priorities often focus on policy objectives, service delivery, and social responsibility rather than purely financial returns. When these institutions enter the capital markets, whether through partial listing or bond issuance, they are exposed to investor scrutiny and market discipline. This transition offers valuable lessons about governance, transparency, and the intersection of economic objectives with financial performance.

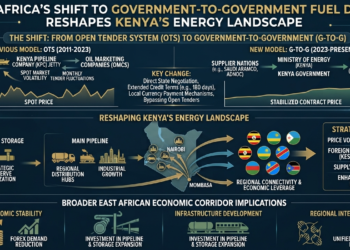

A current example is the Kenya Pipeline Company (KPC) IPO. In January 2026, the Government of Kenya launched the largest IPO in the country’s history by offering 65% of KPC’s equity to the public. The offer comprises 11.81 billion ordinary shares priced at ksh 9.0 per share. The state will retain a 35% strategic stake. By bringing such a strategic asset to market, the government is converting public infrastructure into an investable instrument while retaining policy influence.

One key shift for public enterprises entering the market is the alignment of internal incentives with investor expectations. Decision-making that was once driven solely by administrative priorities must now consider profitability, cash flow stability, and long-term asset management. Procurement practices, capital expenditures, and operational efficiency are no longer just about compliance, they directly affect market valuation and investor confidence. For management, this introduces a new layer of accountability and a more measurable performance framework. Investors, for their part, evaluate these entities differently than traditional private firms. Public enterprises often possess monopoly characteristics or operate in regulated sectors, providing predictable cash flows that appeal to long-term portfolios. However, partial state involvement can introduce complexities, such as policy-driven decision-making or slower operational adjustments. Investors must balance the stability and defensive qualities of these assets with the potential for governance-related volatility. Risk assessment becomes as much about institutional credibility as it is about balance sheet metrics.

From a broader market perspective, listing or partially listing public enterprises enhances economic infrastructure as an investable asset class. It allows capital markets to channel domestic and institutional savings into sectors that are critical for national development, such as utilities, energy, or logistics. By transforming public assets into market-accessible investments, economies can diversify the instruments available to pension funds, insurers, and retail investors, while fostering financial literacy and engagement. There is also a governance benefit embedded in the process. Market participation requires disclosure, audit compliance, and board accountability, which can improve operational transparency and strategic decision-making over time. Public enterprises are thus incentivized to adopt financial discipline that may not have been previously enforced through internal administrative systems.

Integrating public enterprises into capital markets is more than a financing strategy; it is a framework for aligning organizational governance with investor expectations. Done thoughtfully, this approach strengthens both the enterprise and the broader financial system, creating sustainable avenues for capital deployment and economic growth.